A Car Crashes Into Your Home. Your Insurance Says It’s Not Covered. Now What?

Imagine sitting at dinner when suddenly a car crashes through your living room wall.

You call your homeowners insurance company expecting help.

Instead, they say:

“This damage isn’t covered under your policy.”

Many homeowners assume that means they’re stuck paying for the damage themselves. In reality, that’s often not true.

There is another path to recovery called subrogation.

Understanding how subrogation works can make the difference between a denied claim and getting your property fully repaired.

What Is Subrogation in Insurance?

Subrogation is the legal process where an insurance company pays for damages and then seeks reimbursement from the party responsible for the loss.

In situations where a driver crashes into your house, the driver’s auto insurance policy is typically responsible for the property damage, even if your homeowners policy initially denies coverage.

This means your insurance company may still be able to pay you first and pursue the at-fault driver’s insurer afterward.

In simple terms:

Driver crashes into house →

Home insurance pays you →

Home insurance recovers the money from the driver’s auto insurance.

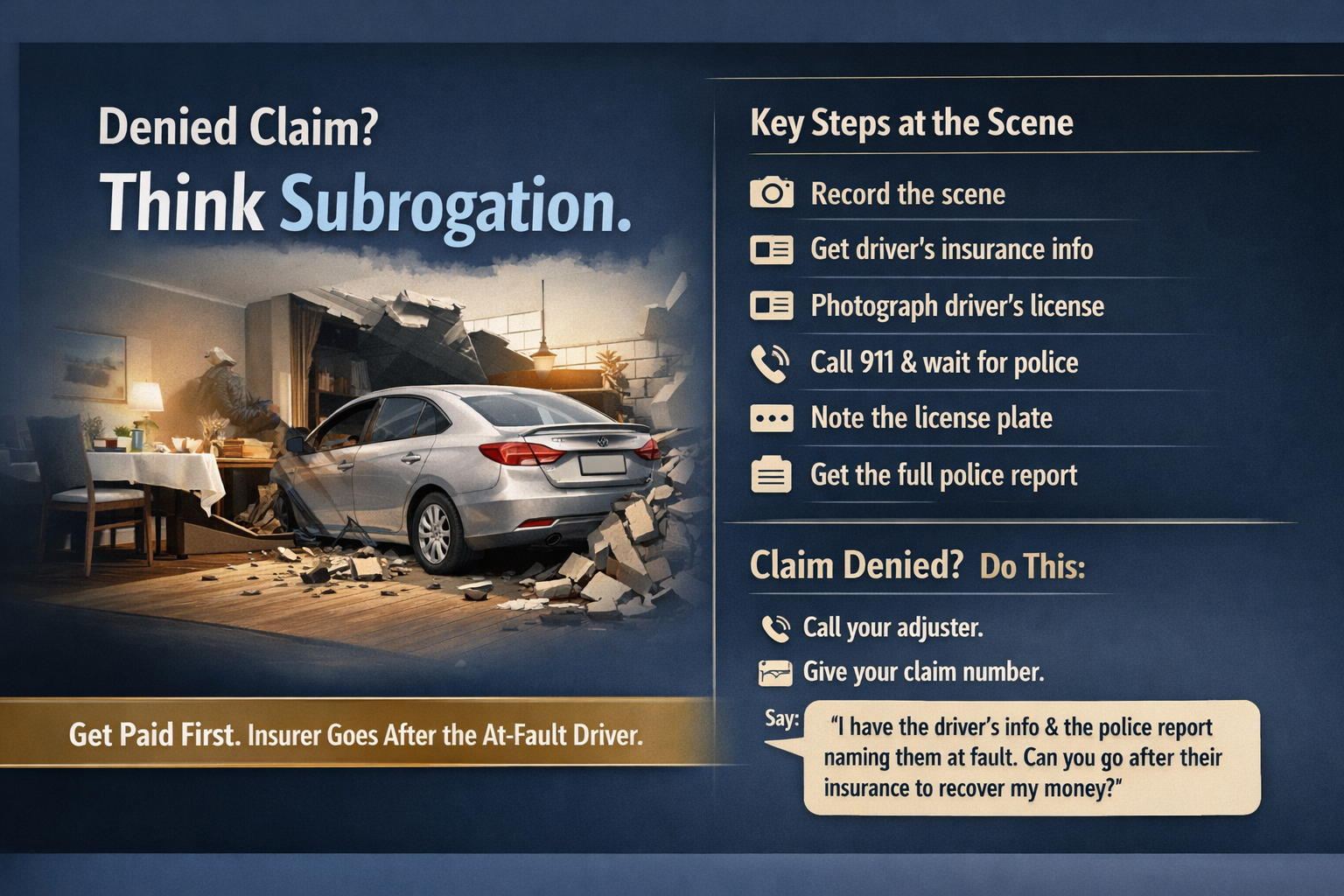

What To Do Immediately If a Car Crashes Into Your Home

Proper documentation can determine whether your claim succeeds or fails.

Take these steps immediately after the crash if it is safe to do so.

1. Start Recording Immediately

Use your phone to record video of the vehicle, damage to the property, and the driver if possible.

2. Get the Driver’s Auto Insurance Information

Ask for their insurance card and take a photo of it.

3. Photograph the Driver’s License

This ensures you have accurate identity information for the claim and police report.

4. Call 911

Report the crash immediately and wait for police to arrive.

After making the call, continue documenting the scene.

5. Record the License Plate

If the driver attempts to leave or flee the scene, capturing the license plate number can be critical to identifying the at-fault party.

6. Obtain the Police Report

The following day, call your local police department’s non-emergency line and request instructions on obtaining the full accident report.

7. File Your Insurance Claim Quickly

Submit the claim to your homeowners insurance company within 1–3 days.

Provide them with:

• Driver’s insurance information

• Photos and videos of the crash

• Police report case number

• Driver’s license photo

• License plate information

What If Your Home Insurance Denies the Claim?

Even when a homeowners policy initially denies coverage, the claim may still be resolved through subrogation.

Contact your adjuster or their manager and explain that you have full documentation of the at-fault driver.

You can say something like:

“I understand the damage may not be covered under my policy, but I have the driver’s insurance information, their license, the license plate, video of the accident, and a police report naming them at fault. Will the company pay my claim and pursue the driver’s auto insurance through subrogation?”

In many situations, the insurer may decide to:

Pay for the repairs Pursue the at-fault driver’s insurance company afterward Recover the funds they paid you

When insurers know they can recover their money, claims often move faster.

Why Subrogation Can Change a Denied Claim

Insurance companies are far more likely to approve payment when they know another insurer is responsible for reimbursement.

By providing clear evidence of fault, you allow the carrier to:

• Recover the claim payout

• Pursue the responsible insurer

• Avoid absorbing the loss

That financial incentive often changes how the claim is handled.

When to Call a Public Adjuster

Claims involving third-party liability can become complicated quickly.

Disputes often arise regarding:

• Fault determination

• Coverage applicability

• Claim valuation

• Responsibility between insurers

At SAPIA – Seth Allen Public Insurance Adjusters, we help homeowners navigate complex claim strategies like subrogation to recover funds on claims that were originally denied.

Our firm represents policyholders—not insurance companies—and works to ensure property owners receive the compensation they are entitled to.

Need Help With a Property Insurance Claim?

If your insurance claim has been denied or mishandled, professional representation can make a significant difference in the outcome.

SAPIA – Seth Allen Public Insurance Adjusters

Phone: 210-988-6118

Email: claim@sapublicadjuster.com

Website: https://sapublicadjuster.com

We help homeowners across Texas navigate property insurance claims with precision, strategy, and confidence.

Leave a Reply